Energygamer's Profile

Energygamer's Posts

http://seekingalpha.com/article/2394765-3-reasons-why-falcon-has-huge-upside-potential

3 Reasons Why Falcon Has Huge Upside Potential

Disclosure: The author is long FOLGF. (More...)

Summary

- Falcon's share price is trading at depressed levels even though it has world class projects on its books.

- Independent consultants have predicted big quantities of oil and gas in Australia.

- Falcon's founder has pedigree as he has had great success with penny stock energy companies in the past.

The first reason is obviously where the share price is trading at the moment. Falcon Oil & Gas Ltd (OTCPK:FOLGF) is trading at just over $0.14 at the moment which is very near its all time low of $0.09 per share. However, back in 2008, Falcon traded at over a dollar a share because of its activity in Makó Trough in Hungary. To cut a long story short, Exxon Mobil (NYSE:XOM) (one of the biggest oil companies in the world) pulled out of the operation in 2010 and this effected the share price negatively. Falcon has not recovered since then but I firmly believe the situation will change for Falcon in the near future. Let's explore why.

Instead of having one world class project on its books, Falcon actually has three. Along with the Makó Trough in Hungary where the current drilling partner is NIS (Naftna industrija Srbije jsc), Falcon also holds 4.6 acres in the Beetaloo Basin in Australia (recently farmed out a huge deal) and 7.5 million acres in the Karoo in South Africa. These projects are far bigger than the Makó Trough in Hungary and since they are still in the development stage (especially South Africa), their potential definitely hasn't been reflected in the share price yet. The picture below shows the locations of their present assets.

Source: Company Website

Secondly the Ryder Scott report came out in 2010 and the report predicted best estimates of 19 billion barrels of oil and 64 trillion cubic feet of Gas in the Australian Beetaloo Basin Property. Ryder Scott are extremely reputable petroleum consultants who evaluate oil and gas properties and independently certify petroleum reserve quantities. If Falcon only produced 10% of the estimates predicted by Ryder Scott, this would still result in a huge move in the share price.

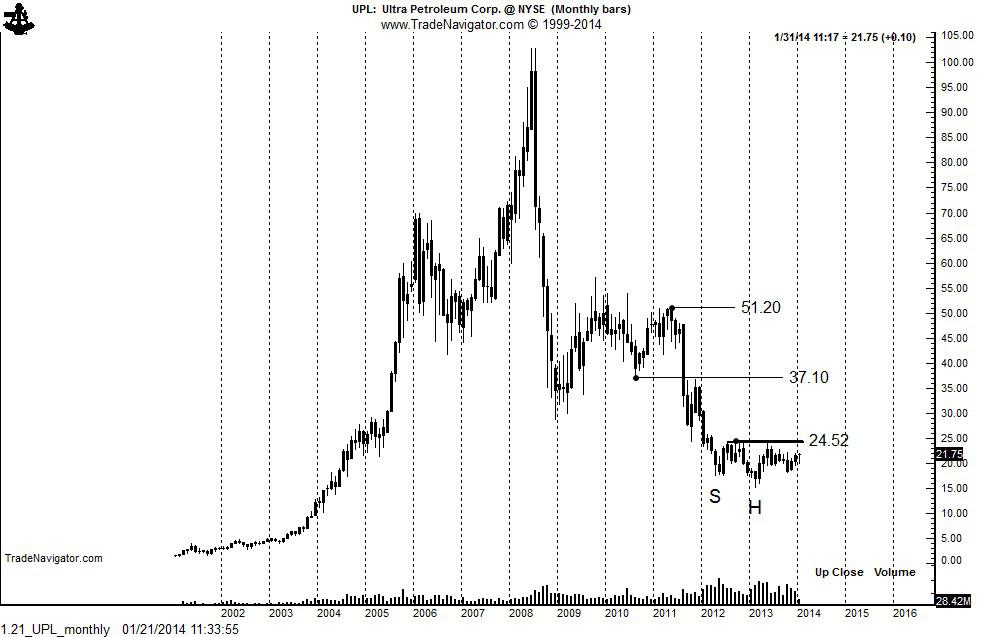

Thirdly is the pedigree behind the company. The founder of Falcon is Marc Bruner and even though he resigned as Falcon CEO in 2010, he has had great success with another energy company called Ultra Petroleum (NYSE:UPL). Between the year 2000 and 2008, Ultra Petroleum went from $0.20 cent a share to a split adjusted $200 a share equating to a 1000 multiple gain of your investment in eight years. The chart below shows what can happen a penny stock when things work out..

(click to enlarge)

In saying all the above, micro cap stocks such as Falcon also carry some risks which should be discussed.

1) Falcon has 921 million shares outstanding. This seems high and implies that dilution has already taken place. Any further dilution would negatively effect the share price going forward.

2) Micro Caps are not liquid stocks and penny stocks like these can be very difficult to get out of. For example, if Falcon plummets and you want to get out, you may not be able to get out until a buyer shows up for the shares you want to offload.

3) If Falcon's drilling partners were to bail out or run into unforeseen challenges such as infrastructure or financial problems, this would be devastating for Falcon as confidence would be lost in the projects and as a result they would find it very difficult to attract new partners.

Where can Falcon go from here?. One thing is sure. Falcon only needs to strike it big in one of its projects. That would be sufficient to drive the stock easily over $10 a share. However if 2 or 3 of its projects turn out to be successful, we definitely could be dealing with another Ultra Petroleum on out hands. Fingers crossed.

Editor's Note: This article covers a stock trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Hi all,

Does anyone have an update on the recent Falcon meetings organised through proactive investors?

Soly - looking at the trades from Friday, I noticed that 429,000 shares were purchased by or through Morgan Stanley. Is this the start of institutional buying ? Any insight ?

I believe that until we receive some positive drilling results (not necessarily full production), the sp will continue to lag due to lack of confidence and investor fatigue. The best near term hope is Hungary then the initial wells in Beetaloo. Hopefully the granting of permits in SA will help, followed by a farmout agreement without protracted delays. The long 5 year timeframe for the project in Australia is having an impact on the sp. From previous experience investing in development stage oil companies, the sp will rise rapidly once progress is been made on drilling, testing etc with regular updates from the company. This is all about giving confidence to the market and the management must deliver within reasonable timeframes.

Confidence is delivery and communication !