DABOSS's Profile

DABOSS's Posts

This first step is significant for a small company like UNXL and was quite a surprise to most investors here, I imagine.

So besides having the ramp to look forward to in 2017, investors now have this MOU to factor into the equation.

Yes, we will not have anything definitive for about 3 months, but the fact that UNXL has the attention of a major player like GIS-Foxconn is a rousing endorsement for their future.

The increased volume with pricing sideways tells me someone is positioning or converting warrants, so as to be positioned if and when they finalize this deal.

Rather exciting developments, imo.

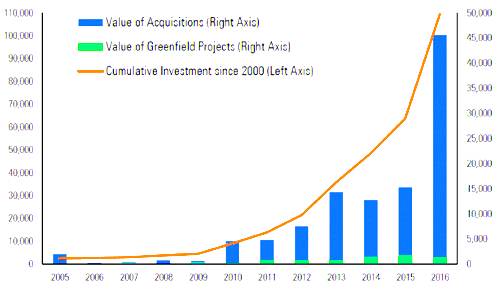

China Goes on an M&A Diet

A decade-long trend of the China government encouraging Chinese businesses to expand globally by acquiring resources, advanced technologies, and distribution channels overseas is hitting a speed bump.

Chinese direct investment into the U.S. hit a record $45.6 billion in 2016, nearly tripling the amount in 2015, including $36 billion invested by private investors. The average deal value rose sharply from $90 million in 2015 to $321 million in 2016 although the total number of completed investment projects by Chinese investors decreased from 169 to 142.

Some eye-catching deals included Haier’s $5.4 billion acquisition of GE’s appliance business, Lexmark for $2.5 billion, and Vizio for $2 billion. Some of the transactions involved an unprecedented level of leveraged financing among Chinese buyers.

The dramatic increase in the Chinese interest in U.S. assets caused political concerns in the U.S., especially in the semiconductor industry. In 2016, several deals were either blocked by or abandoned due to the pressure from the Committee on Foreign Investment in the United States (CFIUS).

A proposed acquisition of Royal Philips NV of an 80.1 percent interest in its Lumileds light business to a Chinese private equity consortium was blocked by CFIUS in January 2016 due to concerns about Chinese control over dual-use semiconductor technology involved in making LEDs. Fairchild Semiconductor International Inc. rejected an offer from a consortium, comprised of China Resources Microelectronics Ltd. and Chinese private equity firm Hua Capital Management Ltd. citing CFIUS concerns. Former President Obama blocked the proposed acquisition of the U.S. business of German semiconductor company Aixtron SE by Chinese investor Fujian Grand Chip Investment Fund LP for $752 million, leading to the termination of the entire transaction.

The strong growth of offshore investment did not come without political risks in China either. The sudden outflow of foreign currency through outbound acquisitions put some pressure on China’s foreign currency reserve, which is closely monitored by the Chinese government with wary eyes.

Starting from the second half of 2016, it has become clear that the Chinese government is poised to tighten its reins on outbound investments. Many investors started to receive interview requests and the filing process to obtain foreign currency slowed down significantly.

In a Q&A statement published in late November 2016, China officials announced offshore M&A transactions are subject to additional governmental scrutiny. They include outbound investment by limited partnerships which are popular with private equity and VC finds in China as well as investments by newly set-up companies with recently received capital contributions.

Various local government agencies also implemented rules restricting capital outflow through overseas acquisitions. The recent actions at local level indicate that all overseas acquisitions going forward must meet the new criteria. For example, the investment needs to be seen as strategic and aligned with the Chinese investor’s core business.

We expect formal rules will be released in the near future to provide legal support for case-by-case reviews. Officials also announced additional reviews over exchanges of more than $5 RMB million versus $50 million in the past. Starting July 1, 2017, all financial institutions in China also must report any cash transactions over 50,000 RMB (approximately US$7,200) or overseas transfers over 200,000 RMB (US$29,500).

Many U.S. companies with recent experience working with potential Chinese investors in M&A deals have shared the same frustrations. After several months of conference calls, a deal seems to be going smoothly until all of a sudden, the Chinese investor calls to say that the promised signing or closing has to be delayed due to some new restrictions on currency exchange or a notice from CFIUS.

Given the recent uncertainties, potential sellers or targets should take a number of steps. For example they can protect themselves by conducting a quick due diligence on the potential buyer and negotiate a binding agreement, requesting a small earnest deposit before engaging a legal counsel or investment bank.

Most analysts believe that the current restrictions are temporary, merely aiming at preserving China’s foreign currency reserve and discouraging speculative transactions without commercial substance in light of the current economic uncertainties. In the long run, those restrictions could either be modified or lifted when the foreign currency reserve in China or the RMB’s exchange rate stabilize.

Item 1.01 Entry into a Material Definitive Agreement.

On January 16, 2017, Uni-Pixel Displays, Inc. (“Displays”), a subsidiary of Uni-Pixel, Inc. (“UniPixel” or the “Company”) entered into a Memorandum of Understanding (“MOU”) with General Interface Solution Limited, a Samoa corporation (“GIS”), to engage in a strategic project regarding the manufacture of XTouch metal mesh sensors (the “Proposed Transaction”). The Proposed Transaction is contingent on the negotiation and execution of definitive agreements by the parties and other customary conditions. The term of the MOU shall be for three months while the parties negotiate the definitive agreements, but upon execution of the definitive agreements, the MOU shall terminate. The term of the Proposed Transaction shall be for three years, during which time Displays shall sublicense to GIS technology for the design and manufacture of XTouch sensors to be incorporated into touch module products and/or to be separately sold by GIS to third parties. Displays will also provide training and technical support to GIS for such design and manufacture. GIS shall make a $6 million cash investment within a month of execution of the definitive agreement. GIS shall also pay a royalty to Displays equal to 20% of sensor manufacturing cost for the sensors to be incorporated into touch module products and 30% of sensor sales prices for the sensors separately sold to third parties. However, there shall be no royalties applied to (a) the first 150,000 sensor units manufactured in 2017 and sold to other parties and (b) the first 300,000 sensor units manufactured in 2018 and sold to other parties.

Displays shall also lease to GIS a manufacturing pilot line / limited production line based in Display’s facility in Colorado Springs, Colorado. This manufacturing line will be leased to GIS until the earlier of (x) the establishment of a separate GIS facility and equipment or (y) expiration of the definitive agreement. After the term of the lease of the manufacturing line, GIS will have the option to extend the lease agreement of the manufacturing line for the manufacture of sensors in Colorado Springs for an additional payment determined at the time of lease extension with such payment not to exceed the average annual payment of the original lease. Displays shall be obligated to purchase from GIS, at GIS manufacturing cost plus 20%, the following minimum quantities of XTouch sensors:

1. 2017 – 1 million units

2. 2018 – 1.5 million units

3. 2019 – 2.0 million units

GIS will have no royalty obligation to Displays for the sensors that GIS sells to Displays. Minimum quantities will be contingent on Displays and GIS agreeing on manufacturing cost. Displays and GIS will meet on a quarterly basis to review manufacturing costs.

The parties shall also work in good faith to enter into a separate advanced technology development agreement targeted primarily at touch sensor modules for the flexible/foldable display market.

The full text of the MOU is furnished as Exhibit 10.1 and is incorporated herein by reference. The foregoing description of the terms of the MOU is only a summary of the material terms of the MOU, does not purport to be complete and is qualified in its entirety by reference to such exhibit.

With the ramp underway and with the $6M cash infusion from the GIS partnership, might they eclipse the $8M threshold?

This small US based, high tech manufacturing company just stepped onto center stage in the penny stock world.

I imagine the market is awaiting the final signing of this agreement between GIS and UNXL.

The volume indicates the stock is moving into stronger hands and preparing itself for a move up, given the enormity of this decision by the asian company GIS/Foxconn to secure US manufacturing entities.

This could morph this company into the stratosphere much faster than the already announced design wins in 2016.

Might UNXL pick up a significant portion of GIS's ongoing business and increase the rate of the ramp from it's already steep incline?

Well worth the wait. Patents, Products, Partners and Global Markets !

I have never seen this designation on UNXL prior to this.